Build a TIPS Bond Ladder: Spend the First Decade, Let Equities Ride

By Lauren Boland | June 5, 2026

Hey Proofers! Today I'm introducing the TIPS bond ladder, a.k.a. the "improved equity glide path." You can now carve off a slice of your portfolio as a set of inflation-protected Treasury bonds, each maturing in a specific future year, and FIREproof will treat their coupons and matured principal as real-dollar cash flows that are insulated from rebalancing.

Instead of selling stocks during the scary opening years of retirement, you fund spending from a bond that matures that year for a known, inflation-adjusted amount. The equity sleeve gets to compound untouched through the worst of the sequence-of-returns window. Planners have a name for the broader idea, the "bond tent" or rising equity glidepath, and it shows up again and again in the research, from Wade Pfau to Michael Kitces to Karsten "Big ERN" Jeske to the 2025 Financial Analysts Journal TIPS-ladder paper. Now you can backtest it against the same historical and Monte Carlo engine you already use for everything else.

Why a ladder, and why TIPS

The single biggest threat to a retirement plan isn't a low average return. It's a bad sequence of returns. A 35% drawdown in year 2 of retirement, while you're also pulling 4% out to live on, does damage that a 35% drawdown in year 25 simply doesn't. The research is consistent on this: sequence risk is overwhelmingly concentrated in the first 10-15 years. Survive that window and the plan almost always makes it.

Michael Kitces calls the window around your retirement date the "retirement red zone" (roughly the five years before through the first decade after you stop working), and explains why it's so dangerous with what he calls the portfolio size effect: your nest egg is at its largest dollar value at exactly the moment a bad return does the most damage. As he puts it, "a 'mere' 20% decline on a portfolio in a bear market evaporates 5 years' worth of spending at a 4% withdrawal rate." His conclusion: "the way to manage the danger is simply to take the least risk with the portfolio when it is the largest."

That's the whole idea behind a bond tent: build up an extra slice of bonds in the years approaching retirement, then deliberately spend it down through early retirement, so your equity allocation dips at the danger point and rises again afterward. The bonds aren't there to juice returns (Kitces describes them as "volatility dampeners"); they're there to carry your spending while equities sit out the most fragile years. Once you're past that first decade, in his words, "good returns will have already carried the retiree past the point of danger, and bad returns at least mean that good returns are likely coming soon."

A bond ladder attacks that window directly. You buy a series of bonds, one rung per year, each maturing in a specific year and promising a known payout. String the rungs across the early years of retirement and you've immunized that span: when a rung matures, it funds that year's spending, so you never have to sell equities into a bear market. By the time the ladder is spent, the dangerous window has passed and the equity sleeve, which you never touched, has had years to recover and grow.

Why TIPS specifically? Because a plain nominal ladder still leaves you exposed to a 1970s-style inflation shock right in the middle of the rung years. TIPS (Treasury Inflation-Protected Securities) return real principal. You enter "$40,000 in today's dollars" and the bond pays out $40,000 of purchasing power whenever it matures, regardless of what inflation did along the way. That lets FIREproof fund a fixed real spend with confidence on every single historical cycle, even the high-inflation ones.

Even a careful skeptic of the heavily-marketed "Safety First" school, Karsten "Big ERN" Jeske of Early Retirement Now, concedes the core idea in his Safety First SWR series: "A partial shift to safe assets like TIPS and annuities can be worthwhile for most retirees." His own backtests show the approach "helps in the Sequence Risk worst-case scenarios," outperforming a static 75/25 baseline even in the 10% worst sequences, which is exactly the point of a ladder. It's insurance that pays off precisely in the bad-sequence cases that sink a plan, at little cost in the good ones. He's also refreshingly blunt about the catch: the longest TIPS maturity is only 30 years, so a ladder by itself doesn't solve longevity past three decades. That's precisely why FIREproof pairs a finite ladder with a compounding equity sleeve: the ladder handles the fragile opening years, the equities handle the long tail.

What FIREproof actually models

A ladder isn't just a relabeled bond fund. Each rung is a real bond with its own maturity year and coupon, and it behaves differently from the rest of your portfolio in three ways:

- Rungs are never rebalanced. They're a finite carve-out that stays put until maturity. Your normal equity / bonds / cash / gold targets apply to the rest of the portfolio.

- Maturity cash funds spending first. The year a rung matures, its principal (your real par adjusted for that cycle's inflation) lands as cash and is spent before anything is sold from equities.

- Rungs are held to maturity. A rung is never sold early to plug a shortfall, so size your ladder with a little buffer.

One ladder can span multiple accounts (a few rungs in your Roth, a few in a Traditional IRA, a few in a taxable brokerage), exactly how a real tax-aware ladder gets placed. FIREproof handles the taxes of each placement correctly (more on the brokerage wrinkle below).

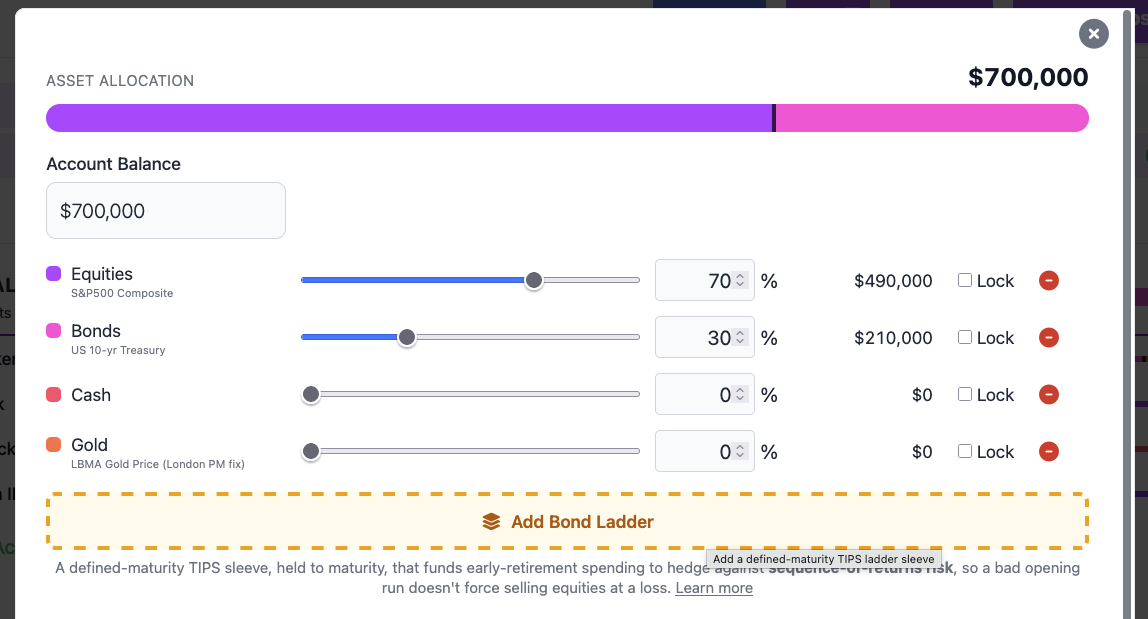

Building a ladder

Ladders are configured per account. Open any multi-asset account (Brokerage, Roth, Traditional IRA, a 401k, HSA), click Edit Allocation, and hit Add Bond Ladder. Cash-only Checking and Savings accounts can't hold one, so the button only appears where it makes sense.

Screenshot: the Edit Allocation modal on a Brokerage account, scrolled to the Bond Ladder section with the Add Bond Ladder button highlighted. The allocation sliders manage the non-ladder dollars; the ladder has its own editor.

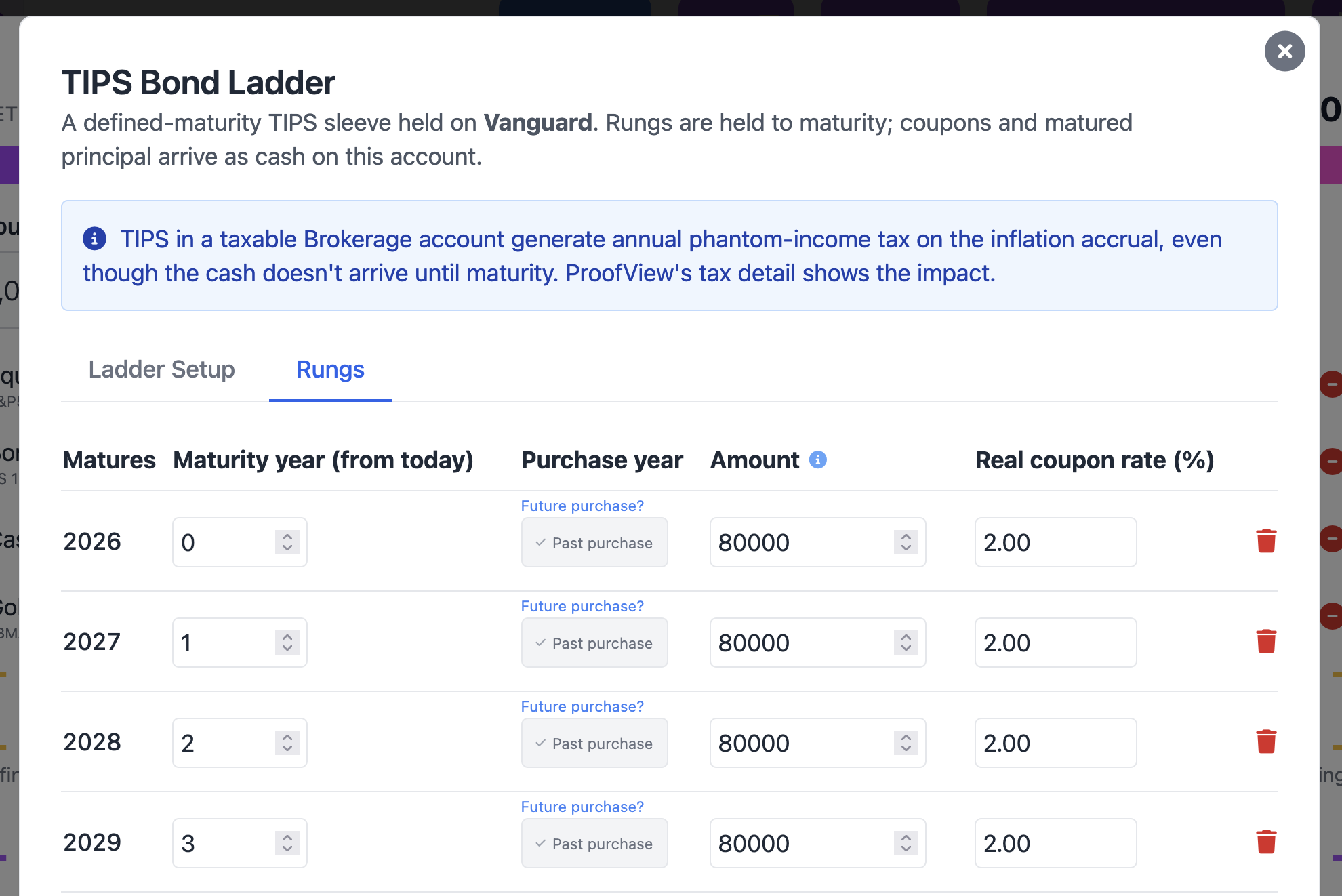

The editor has two tabs: Ladder Setup for the policies and Rungs for the bonds themselves. In the Rungs tab, click + Add rung for each year you want to cover and set:

- Maturity year: when the rung pays out (the editor shows the calendar year alongside).

- Par (real $): the face value in today's dollars; it's grown to nominal at maturity by each cycle's inflation.

- Real coupon rate: the rung's real yield (e.g. 0.02 = 2%).

- Purchase year: leave at 0 for bonds you already hold, or set a future year to schedule the purchase (more below).

Screenshot: the Rungs tab, showing a row per rung with Maturity year, Par, coupon, and Purchase year columns.

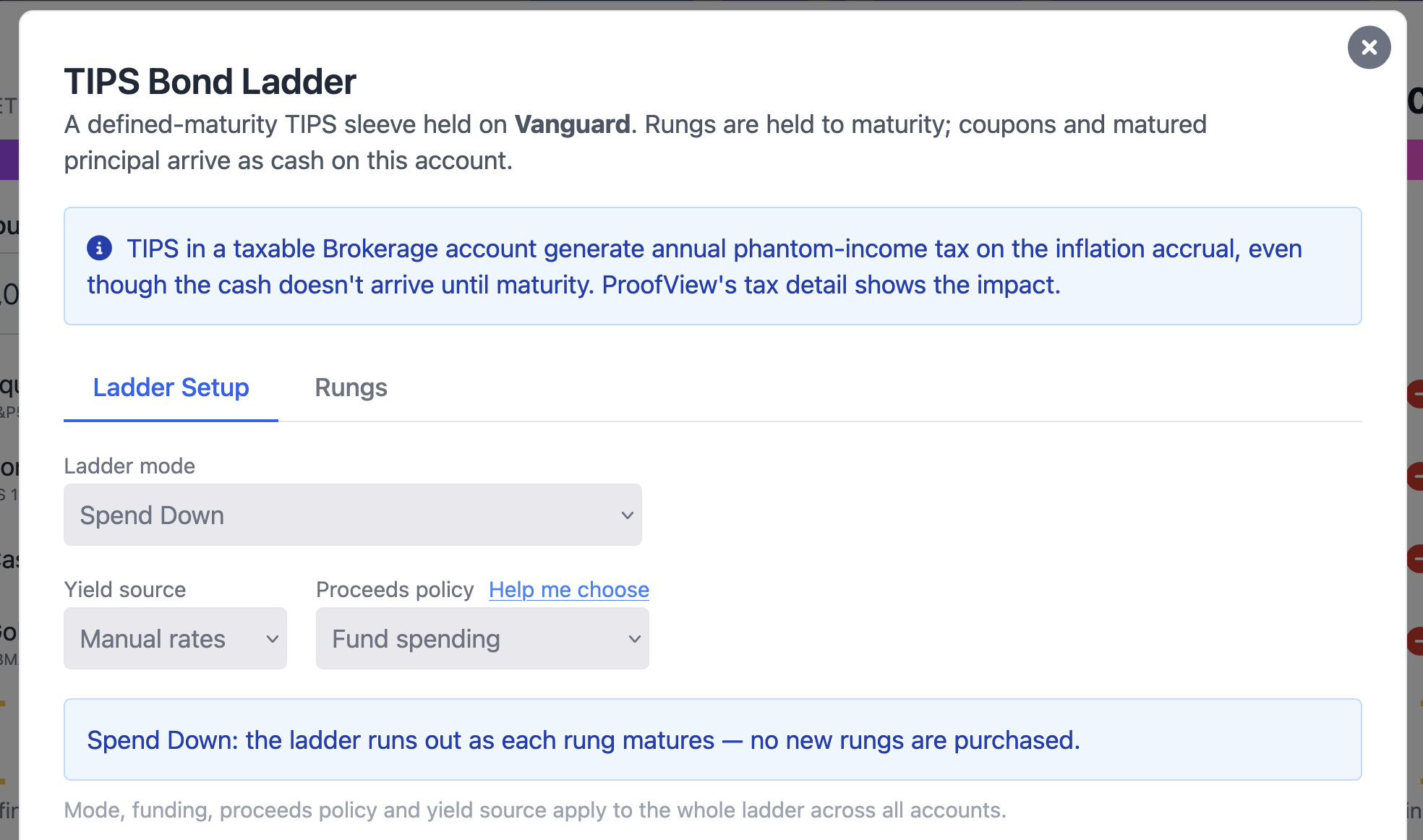

Three modes: how long should the ladder last?

The top of the Ladder Setup tab has a mode selector. This is the single most important choice, because it decides what happens when a rung matures:

- Spend Down (the default): a finite ladder. Rungs mature, fund spending, and are gone, then your equity sleeve takes over. This is the canonical "improved equity glide path": the ladder carries you through the opening years, then gets out of the way.

- Continuous (perpetual): every maturing rung is replaced with a new long-dated one, so the ladder slides forward forever as a permanent inflation-protected income floor. For when you want a lifelong hedge, not a finite bridge.

- Continuous, then Spend Down: maintain the ladder up to a sunset year (e.g. age 85), then stop replacing rungs and let it drain. You get a floor for the years you most want certainty, wound down gracefully after.

Both continuous modes use a forward-horizon slider: "always keep N years of rungs in front

of me" (1–50, default 10). Each maturing rung is replaced with one maturing N years out, keeping

the structure intact year over year.

Screenshot: the Ladder Setup tab. The three-mode selector sits up top, with the forward-horizon slider, yield-source toggle, proceeds policy, and funding-source picker below. The continuous-only controls appear once you pick a continuous mode.

Yield source: Fixed rate, or use historical data

Each ladder picks one of two yield-source modes:

- Manual: your entered coupon rate applies across every cycle. Good for "what if I locked in these yields?" sensitivity tests.

- Historical TIPS: each cycle uses the real TIPS yield that actually prevailed at its start year. Good for realistic backtesting (a 1985 retiree and a 2010 retiree bought very different ladders). Constant-Returns and Monte Carlo modes fall back to the most recent real yield.

What happens to the cash: proceeds & funding policies

Two policies govern the money moving through the ladder. The proceeds policy decides what happens to a rung's matured cash after spending:

- Fund spending (default): spending pulls from the matured cash first; any leftover stays as surplus.

- Reinvest into ladder: surplus mints a new rung at the far end.

- Rebalance to equities: surplus goes into your equity sleeve.

In a continuous mode, each replacement rung costs money. Matured principal covers part of it; the funding-source policy covers the rest:

- Surplus maturity cash only: fund replacements purely from matured principal. Cheapest, but if yields don't keep pace the ladder shrinks a little each year (the editor warns you when that's likely).

- Surplus cash, then sell equities: top up by selling equities. Holds the horizon at full size at the cost of drawing down the equity sleeve.

- Pull from a specific account: recycle maturity cash first, then draw from a named account (e.g. a savings reserve) to cover the gap.

If funding falls short, the replacement is sized down (or skipped) rather than failing the cycle, and a Funding shortfalls row in Proof View shows you exactly when and by how much.

Building a ladder over time (the pre-retirement play)

You don't have to own the whole ladder on day one. Give a rung a purchase year greater than 0 and it becomes scheduled, bought in that future year rather than today. This is the pre-retirement build-out: divert money into a ladder in the years before you retire, then spend it down once you're in.

You build it from two pieces you already have: an income Adjustment (a job/side-hustle contribution, or a plain contribution) that deposits into the rung's account, plus a scheduled rung whose funding source is surplus maturity cash only or pull from a specific account, so it draws from that accumulated cash when its purchase year arrives.

A "Build out a ladder" auto-fill saves you hand-entering 30 rows: give it a span of build years, a maturity offset, a par per year, and a coupon, and it generates the rungs, e.g. "$40k/yr for 5 years, each maturing 10 years later." The generated rows are normal, editable rungs.

Screenshot: scheduled rungs wearing their amber "Scheduled for year N" badges, sorted to the top of the table, alongside the Build out a ladder auto-fill panel mid-fill.

A tax wrinkle worth knowing: phantom income

The IRS taxes TIPS inflation adjustments in the year they accrue, even though the cash doesn't arrive until maturity. This is the infamous "phantom income." FIREproof models this: a rung in a taxable brokerage account generates an annual ordinary-interest tax on its inflation accrual, and that income flows through everything downstream (IRMAA, ACA credits, Social Security provisional income, NIIT, your bracket-fill space).

Rungs inside retirement wrappers (Roth, Traditional IRA, 401k, HSA) skip phantom income entirely, which is why tax-aware ladders often live there. FIREproof doesn't block brokerage placement; it just flags the trade-off and shows the dollar cost per year in Proof View.

What you'll see in your results

Run the simulation and head to Proof View. Two views tell the ladder's story.

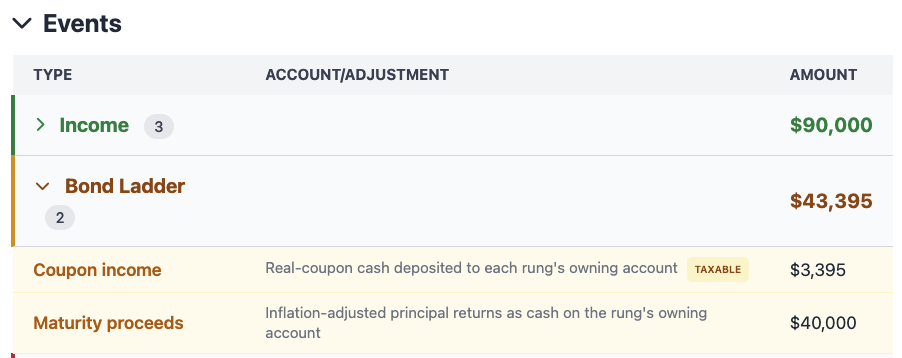

First, the year-by-year Cash Flow drill-down grows a dedicated Bond Ladder group, with rows for whichever apply:

- Coupon income deposited to each rung's account.

- Maturity proceeds: principal landing as cash the year a rung matures.

- Phantom-income tax accrued on brokerage rungs.

- Replacement purchases and Funding shortfalls, for continuous ladders.

- Scheduled purchases and shortfalls, for build-out ladders.

Screenshot: the Bond Ladder cash-flow group inside Proof View's year-by-year Events panel, with the amber-tinted Coupon income, Maturity proceeds, and Phantom-income tax accrued rows for a selected year.

Second, the allocation chart picks up a distinct "Bond Ladder" bucket, separate from regular bonds. This is where the "improved equity glide path" becomes visible: in Spend-Down mode you watch the ladder bucket shrink year by year while the equity share climbs, with no hand-drawn glide path required. (In a Continuous ladder it holds roughly constant instead.)

A worked example: maintain until 85, then drain

Say you hold a $400k TIPS ladder in Continuous, then Spend Down mode, with a forward horizon of 10 and a sunset at age 85:

- Through age 85: every maturing rung is replaced 10 years out, so you always have ~10 years of rungs in front of you and a steady real income floor.

- At age 85: replacements stop. Your proceeds policy takes over. Surplus is held as cash or routed into equities.

- Ages 85–95: the remaining rungs mature one by one, draining the floor to zero by about age 95.

And the outcome you're hunting for across cycles: a meaningfully lower failure rate (because no cycle is forced to sell equities into its opening crash) without a lower median terminal wealth, because in the cycles that didn't crash early, your equity sleeve still got to ride. That asymmetry, fewer bad-case failures at little-to-no good-case cost, is the whole reason this strategy shows up in the research, and now you can measure it on your own numbers.

Limitations & a couple of rules

- Held to maturity. The engine won't sell a rung early to plug a shortfall, so size your ladder with a buffer.

- TIPS only in v1. Nominal bond ladders aren't modeled yet.

- Single-tenor yields. Historical TIPS mode applies one real-yield value to every rung regardless of maturity; a full per-tenor curve is a future enhancement.

- One spending engine at a time. A portfolio can run a TIPS Ladder or a Bucket Strategy, but not both. Both control "where does spending come from," and picking a precedence between them has too many corner cases for v1. Each editor warns you when the other is active.

Wrapping up

The TIPS ladder/tent is a powerful tool for managing sequence risk, and I'm excited to see how you use it. The research on this is pretty strong, and it is frequently talked about in the online spaces that I occupy, so I'm happy to bring it to FIREproof.

As always, I'd love to hear how it goes. Reach out if you hit anything surprising.

-Lauren

Support this project!

FIREproof is now past v1.0.0 and I'm building it as a solo developer. A Pro subscription keeps the lights on and gets you early access to new features as they land. If you've found this useful, it's the best way to say thanks and keep this project moving forward.